“Real Estate Agents, Tech Professionals, Freelancers, Programmer, Software Engineers often have more back tax challenges more than other types of work”

The Complete Guide to Offer in Compromise with IRS.

If you’re in one of these industries you could face tax debt issues – “Real Estate Agents, Tech Professionals, Freelancers, Programmer, and Software Engineers often have more back tax challenges than other types of work. ”

-Sonali Patel, Solvable 2022

Easy Article Navigation

- What is an Offer in Compromise?

- Who’s eligible for an Offer in Compromise?

- What if I am not eligible for an Offer in Compromise and I send in a payment?

- If I am currently in bankruptcy, can I apply for an Offer in Compromise?

- What if I don’t owe the money that IRS claims I do?

- What is a as Doubt as to liability?

- Who are usually the best candidates for Offer in Compromise?

- What is a Minimum Offer Amount for an Offer in Compromise (OIC)?

- The IRS will not let you count these expenses toward dept relief.

- Offering One Total Payment for OIC

- Offering a Payment Plan for OIC

- What do you pay if your offer is based on doubt of liability?

- Do I have to pay an application fee or initial down if my family meets the low-income Certification guidelines?

- What would cause a OIC to be Rejected?

- Are there Any Options Once My Offer has been Rejected?

- What is the level of hassle you’ll face submitting an OIC?

- Is the Fresh Start Initiative Different that an OIC?

- Is it a Good Idea to Hire Professional Help?

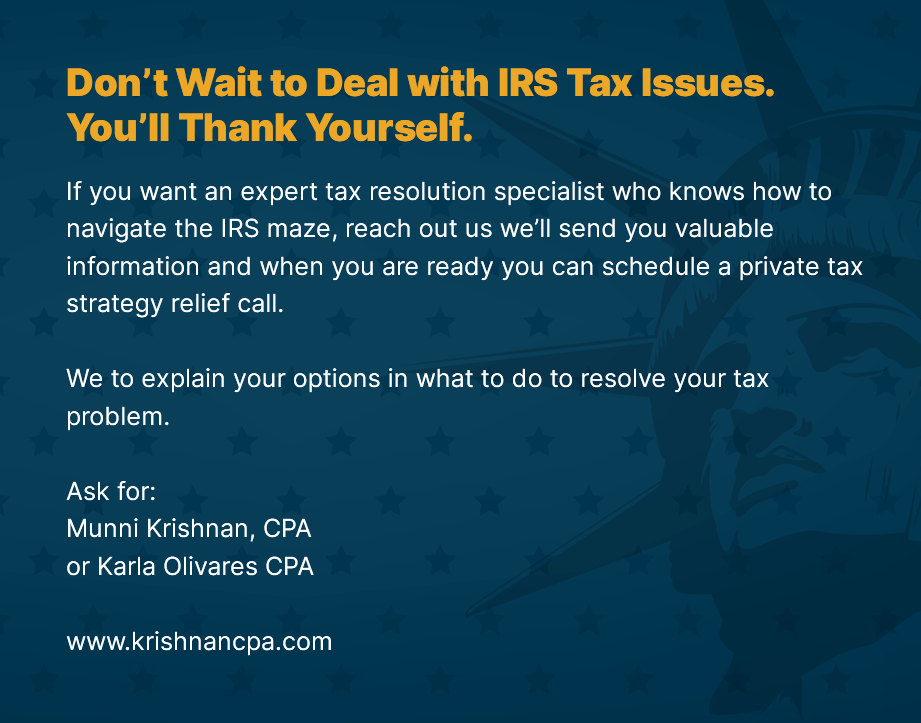

- Don’t Wait to Deal with IRS Tax Issues. You’ll Thank Yourself.

What is an Offer in Compromise?

You may have heard on the radio, TV, and online, that you can settle your tax bill for less than what you owe. But are these claims true? And can you really settle your tax debt without hurting yourself in the long run?

The truth is that though it’s often harder than they claim to settle for less than you owe the IRS, it is possible. If you or your business are getting notices from the IRS that are over $10,000 in debt to the IRS. You might qualify for an Offer in Compromise.

Let’s dive deeper into Offer in Compromise and discover what it is, who can apply, how to apply, offer details, and who can help you navigate the IRS with the best result.

Who’s eligible for an Offer in Compromise?

So, you’re looking for an offer in compromise? Make sure that before your request can be considered by our team of experts – which includes being legally required to file all tax returns and make payment on debts included with this process-you’ve subjected yourself correctly beforehand! Here are some things worth knowing:

- The IRS expects that you file all the tax returns you are legally required to file.

- You have received a bill for at least one tax debt included on your offer.

- You make all required estimated tax payments for the current year.

- Business owners with employees, make all required federal tax deposits for the current quarter and two preceding quarters.

What if I am not eligible for an Offer in Compromise and I send in a payment?

The IRS will apply any initial payment you send with your offer to tax debt and return both the application fee as well. There is no appeal process, so be sure that all your Tax returns are properly filed before sending you Offer in Compromise application.

If I am currently in bankruptcy, can I apply for an Offer in Compromise?

You are not eligible to apply for an offer. Any resolution of your outstanding tax debts generally must take place within the context of bankruptcy proceedings.

What if I don’t owe the money that IRS claims I do?

If you’ve been contacted by the IRS and you have a legitimate doubt that you owe part or all the tax debt you can submit a 656-L Form – this is called Doubt as to Liability.

What is a as Doubt as to liability?

It’s an offer when the taxpayer feels they do not owe a debt, there must be an explanation as to why and any supporting documentation supplied. The reason for doubt should also demonstrate by clear-cut evidence to support their claim.

Who are usually the best candidates for Offer in Compromise?

- You're a retiree on fixed income.

- You’re in legal trouble with the IRS. They’re often looking to settle tax debt instead of causing more red tape with a lawsuit.

- You’re facing bankruptcy because of unpaid taxes.

- You can't pay your tax liability or doing so creates hardship in the form of financial difficulty for yourself and family.

- You meet federal low-income guidelines that aren’t so low these days: under $51,950 for a family of three, under $73,550 for a family of five, and so on.

The federal government weighs your unique facts and circumstances to determine whether you qualify for exceptions. Facts like income, expenses, assets are all considered.

The IRS says that an offer in compromise is most likely going to be approved when the amount offered represents what they expect will end up being collected within a reasonable period time.

You can click here to get more info on IRS guidelines: www.irs.gov/advocate/low-income-taxpayer-clinics/low-income-taxpayer-clinic-income-eligibility-guidelines

What is a Minimum Offer Amount for an Offer in Compromise (OIC)?

The smallest offer the IRS will accept will depend on your financial condition, and you will need to reveal that in detail on Form 433-A (for wage-earners and the self-employed) or 433-B (for businesses).

These forms are required detailed information beyond income and expense.

They will want to know:

- If you have declared bankruptcy

- If you are the beneficiary of a trust, estate, or life insurance policy. Additionally, how much and when you might receive the money from these income sources.

- If you have valuables in your safe deposit box

- The amount of money in your personal bank accounts.

- What kind of credit you have?

- The cash value of your life insurance policies.

The IRS will not let you count these expenses toward dept relief.

- College or any private school expenses

- Charitable contributions

- Voluntary retirement contributions

- Payment on unsecured debts.

After submitting all your financial details, the minimum offer calculation is based at least a year to two years’ worth of income above what it considers acceptable expenses. The IRS will demand you pay something even if your secured debt and expenses exceed your assets.

What’s involved in submitting an offer and how much does it cost?

When you apply for an offer in compromise, it’s important to be prepared with all the necessary documentation and forms, the actual offer and the collection information statement for an individual or business.

Once done, you will send the IRS The application fee for $150 and the first payment of your offer.

Offering One Total Payment for OIC

People offering to pay in one lump sum will pay 20% of the total offer amount. Should the offer get accepted through a written notice the remain balance must be paid in five or fewer payments.

Offering a Payment Plan for OIC

People offering a payment plan would include their first payment in the offer and continue to make that payment until they are contacted by the IRS via mail. Should the offer be accepted, they should continue to pay monthly payments. The payment plan should be paid in full but not take longer that 24 months to pay after you have received your official acceptance letter.

What do you pay if your offer is based on doubt of liability?

You are not required to pay a fee.

Do I have to pay an application fee or initial down if my family meets the low-income Certification guidelines?

People who meet these guidelines do not have to pay the application fee or initial down payment. Monthly income, the size of your family and where you live will determine whether the fee the initial down is required.

What would cause a OIC to be Rejected?

Careful attention to detail is the most important thing when it comes to submitting your OIC. Rejection can happen due any number of reasons, but the most common are these:

- The IRS believes the offer is too low. They have a reasonable doubt that your capability to pay in full is more than your offer based on future earnings. The IRS will counter you the amount they believe you can pay.

- Failing to provide enough documentation of your finances to fully expose your financial condition.

- Your behind on tax your current tax filings. The IRS will believe you’re a poor risk to pay the OIC. In other word, all your tax returns are not in order and correctly filed.

- People who have a criminal record and have been convicted of a serious crime.

Are there Any Options Once My Offer has been Rejected?

Recent numbers from the IRS report that fifty percent of Offers in Compromise are rejected.

There are three options to respond to the IRS once your OIC has been rejected.

- Send a letter in 30 days after rejection proposing a larger amount. When you do it within the 30-day window you don’t have to submit new Form 656.

- After 30 days from rejection, you will have to fill out a new Form 656 to submit a new offer.

- Appealing the rejection requires identifying the part of the rejection you dispute and the reason. When appealing the rejection, you will need to file from 12711within 30 days of the rejection letter.

There are two ways to respond to IRS rejecting an OIC. One is to resubmit an offer. If you, do it less than a month from the first offer, a new Form 656 isn’t necessary, just a letter increasing the amount of money you’re offering.

If you wait longer or significantly change the offer, fill out a new Form 656. To appeal the rejection, file Form 13711 within 30 days of the rejection letter, identifying what parts of the rejection you dispute and providing your reasons.

What is the level of hassle you’ll face submitting an OIC?

It’s a huge headache gathering and meticulously submitting the right paperwork and income information to the IRS. The other hassle is that once you have done all the hard work it can take up to a year and more to get your answer. If you appeal, it will take even longer.

If your offer is accepted you must remain vigilant and stay current with all your tax filing for 5 years, one small mistake, and the IRSL will revoke your agreement and demand payment in full. They don’t mess around.

An OIC also suspends the 10-year statute of limitations the IRS has to collect taxes from you. If it’s been six years since the IRS assessed taxes against you, it has four years left to collect. If it takes a year for your OIC to be considered and it is rejected, the IRS still has four years to collect against you.

The IRS’s 10-year statute of limitations on tax collection is also suspended by an OIC. If it has been six years since it assessed taxes against you. The IRS still has four years to pursue payment from you even if it takes a year for your OIC to be reviewed and it is refused.

Is the Fresh Start Initiative Different that an OIC?

No, they are the same program. The IRS expanded its Fresh Start Initiative in 2012, and OIC acceptance rates have increased significantly from the prior 25–30% level.

The measure raised the threshold for filing a tax lien from $5,000 to $10,000. It gave relief from a few of the penalties that could be imposed in addition to the taxes due. Additionally, it created more favorable OIC conditions and loosened the qualifying rules for paying back taxes on an installment plan.

Is it a Good Idea to Hire Professional Help?

Absolutely! The IRS is NOT on your side. In fact, their overall goal is to collect as much money as they can out of you while they can.

Simply put, the IRS would rather take an Offer in Compromise settlement than to send you to private collections and potentially lose money out of the deal. Plus, if you qualify and get your offer accepted, the offer in compromise will NOT affect your credit score at all.

Doing it on your own can lead to additional stressful mess with the varying complexities involved in the process. Determining what offer to make and learning the whole process is challenging while playing the game of long odds in getting your offer accepted.

Think of it like this- would you represent yourself in the court of law in front of a judge? Probably not. You need some who knows your rights and who’s your advocate – most people would hire an attorney.

Facing the IRS alone isn’t a good idea. You need a tax professional, who not only know tax code but also knows the taxpayer bill of rights and will be your advocate.

Finding a 5-star rated tax resolution specialist that can help navigate the whole process without stress is your best bet. A tax resolution specialist will also be a licensed CPA, Enrolled Agent, or an Attorney.

One of the great things about working with a qualified and local tax resolution firm is that you get protection from the overbearing IRS, letting you sleep better at night knowing you’re on your way towards permanent tax resolution. They can head-off any impending garnishments of your paycheck or levies on your bank account.

Settling with the IRS is a good thing and is often the best answer to dealing with your back tax bill and moving on with your life.

As local CPA Tax Resolution Firm, our mission is to help business owners free themselves from IRS problems.

We encourage all readers facing a tax problem to contact us for a free consultation: www.krishnancpa.com.

Easy Article Navigation

- What is an Offer in Compromise?

- Who’s eligible for an Offer in Compromise?

- What if I am not eligible for an Offer in Compromise and I send in a payment?

- If I am currently in bankruptcy, can I apply for an Offer in Compromise?

- What if I don’t owe the money that IRS claims I do?

- What is a as Doubt as to liability?

- Who are usually the best candidates for Offer in Compromise?

- What is a Minimum Offer Amount for an Offer in Compromise (OIC)?

- The IRS will not let you count these expenses toward dept relief.

- Offering One Total Payment for OIC

- Offering a Payment Plan for OIC

- What do you pay if your offer is based on doubt of liability?

- Do I have to pay an application fee or initial down if my family meets the low-income Certification guidelines?

- What would cause a OIC to be Rejected?

- Are there Any Options Once My Offer has been Rejected?

- What is the level of hassle you’ll face submitting an OIC?

- Is the Fresh Start Initiative Different that an OIC?

- Is it a Good Idea to Hire Professional Help?

- Don’t Wait to Deal with IRS Tax Issues. You’ll Thank Yourself.